.svg)

Stablecoins explained: digital money that holds steady

Stablecoins are digital money that doesn't move when crypto markets do, like a digital dollar designed to stay close to one dollar.

What Are Stablecoins in Simple Terms?

Key Takeaways

- Stablecoins are digital money designed to hold steady value (usually $1) even when other cryptocurrencies swing wildly up and down

- Most major stablecoins are backed by real assets like cash and short term treasuries held in reserves by the issuing companies

- Main uses include fast global transfers, crypto trading, and protecting savings in countries with weak local currencies

- Different designs carry different risks - some stablecoins have lost their $1 peg during market stress, costing investors money

- Regulation is coming with new laws requiring safer reserves and stronger oversight of stablecoin issuers

What is a stablecoin? (Simple Explanation)

Stable coins are digital money that doesn’t move when crypto markets do. Think of them as a “digital dollar on the internet” that lives on a blockchain.

A stablecoin is a type of cryptocurrency designed to maintain a stable value. Usually around one us dollar per coin. Instead of jumping up and down like Bitcoin or Ethereum, stablecoins aim to stay steady.

This digital representation of fiat currency can move 24/7 across the global financial system. No weekends off. No banking hours. But unlike other cryptocurrencies, it’s designed not to change value much.

Most stablecoins peg to something familiar. The us dollar dominates this space. Some link to other currencies or even gold. But dollar stablecoins control the vast majority of the market.

As of mid-2025, the global stablecoin market has grown to hundreds of billions in market capitalization. Almost every major coin connects to the us dollar. This massive scale shows real demand for stable digital money in our increasingly connected world.

Why do stablecoins matter in crypto?

Crypto is known for big swings. Stablecoins are designed to avoid them. They create a calmer corner in the wild world of digital assets.

Here’s why they matter:

- Safe parking space - Traders step into stablecoins when other crypto prices get too choppy

- Bridge to traditional finance - They connect banks, payment systems, and crypto exchanges

- Fast global transfers - Move money across borders in minutes, not days

- Base currency for trading - Most crypto exchanges use dollar stablecoins as their pricing unit

Bitcoin can move 5-10% in a single day. During market stress, it might swing even more. A major stablecoin like usd coin typically stays very close to $1.00. This stability helps traders avoid constant price changes when they want to step aside.

Because stablecoins offer this stable value, crypto exchanges worldwide use them as their main pricing unit. You’ll see trading pairs like BTC/USDT instead of BTC/USD. This keeps funds inside the digital ecosystem without constantly moving money to traditional banking system accounts.

The impact goes beyond trading. Stablecoins affect how money moves globally. They change how people save in unstable economies. They even influence how central banks and governments think about the future of digital currencies.

How do stablecoins stay “stable”?

Different stablecoins try to stay at $1 in different ways. Some hold reserves. Others use smart contracts. Many combine approaches.

Almost all major stablecoins aim for a 1:1 peg to a fiat currency. Most commonly the us dollar. This means 1 coin should equal roughly 1 dollar.

A “peg” is simply a target exchange rate. The issuer or system tries to maintain this rate through various methods. When demand changes, mechanisms kick in to defend the peg.

The basic idea behind reserves is straightforward. For every 1 dollar-pegged stablecoin issued, the issuer should hold roughly 1 dollar’s worth of safe assets. These reserve assets might include cash in bank deposits, treasury bills, or other liquid assets held in separate accounts.

Here’s how supply and demand work in practice. When users want stablecoins, they give dollars to issuers and receive new coins. When they want to exit, they return coins and get dollars back. This creates and destroys coins based on demand, helping maintain price stability around $1.

Some stablecoins also rely on algorithms and incentives rather than full reserves. These designs use code to expand or contract supply automatically. However, such stablecoins can be more fragile when market confidence breaks down.

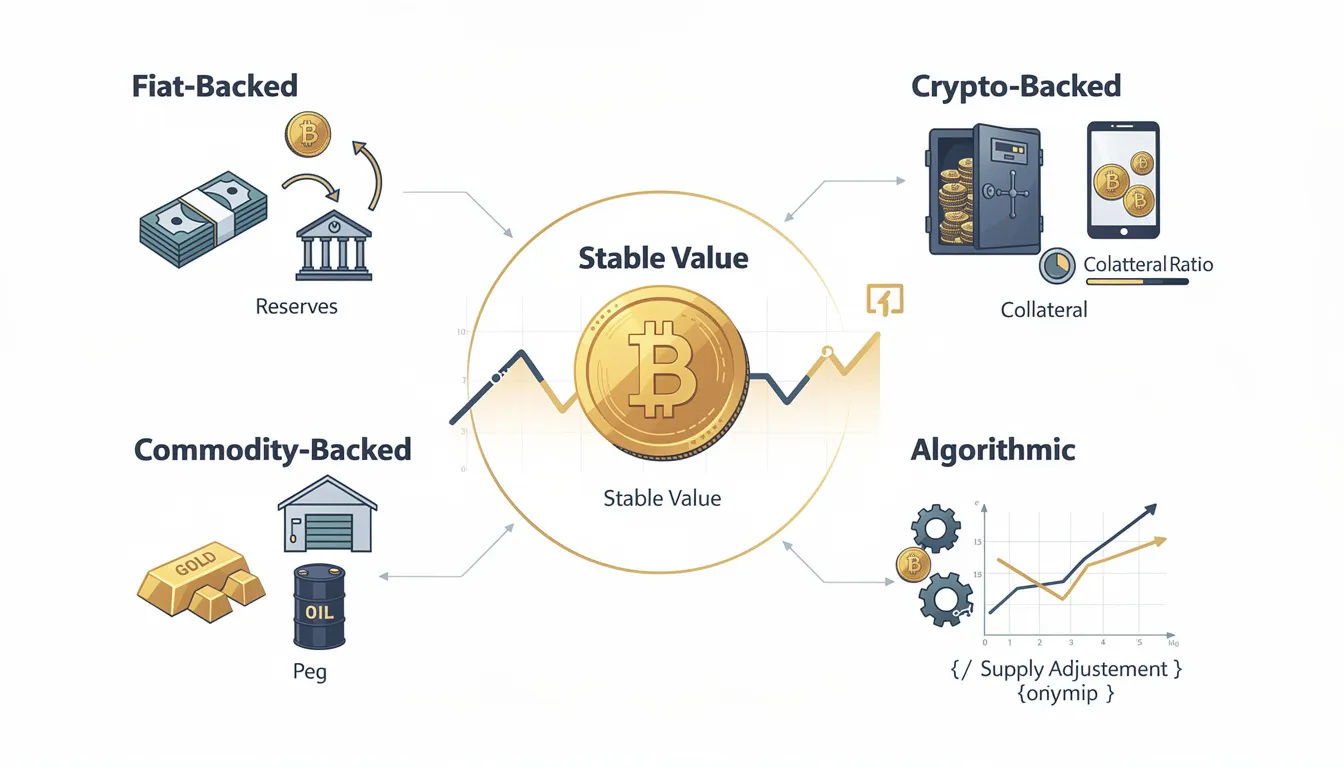

Main types of stablecoins

The key difference between stablecoins lies in what keeps them stable. Some use fiat currency reserves. Others use crypto collateral. A few rely on commodities or complex algorithms.

Four main types exist today:

- Fiat-backed - Reserves of traditional money and cash-like assets

- Crypto-backed - Other cryptocurrencies locked in smart contracts

- Commodity-backed - Physical goods like gold stored in vaults

- Algorithmic - Code and incentives without full reserves

Fiat backed stablecoin designs like USDT and USDC dominate the market today. They hold the vast majority of market cap among all stablecoins. More experimental designs, especially algorithmic stablecoins, have seen spectacular failures in recent years.

Each type brings different trade-offs between simplicity, decentralization, and risk. Understanding these differences helps users choose what fits their needs and risk tolerance.

Fiat-backed stablecoins

These are the simplest to understand. Each coin is backed by traditional money or cash-like assets held off-chain by the issuer.

Popular examples like Tether (USDT) and usd coin (USDC) hold reserves in forms like bank deposits and treasury bills. Users expect 1 coin to equal approximately 1 us dollar based on these holdings.

Here’s the basic process: Users send dollars to the issuer through approved partners. They get stablecoins in return. Later, they can send coins back to redeem dollars. This usually happens through licensed exchanges or payment platforms rather than directly.

Potential issues arise when reserves face problems. If holdings include risky investments, insufficient backing, or unclear auditing, the coin can temporarily fall below $1. This “de-peg” happens when many people rush to sell at once.

Regulators in major markets are moving toward stricter rules. The european union, United States, Singapore, and hong kong sar now require or plan to require safer reserve assets. Monthly audits and strong risk controls are becoming standard for licensed stablecoin issuers operating in these jurisdictions.

Cryptocurrency-backed stablecoins

These stablecoins use other cryptocurrencies as backing, locked in smart contracts on blockchain networks.

DAI provides a concrete example of how this works. Users deposit more than $1 worth of crypto - perhaps $150 of Ethereum - to create 100 DAI coins. Even if Ethereum’s price falls significantly, enough backing remains to support the stablecoin’s value.

This “over-collateralization” acts as a cushion against crypto price drops. You must lock up more value than you create. If you want 100 DAI, you might need to deposit 150-200% worth of Ethereum or other accepted cryptocurrencies.

Smart contracts automatically track market prices through data feeds called oracles. If collateral values fall too far, the system can automatically sell some to protect the stablecoin’s stability. This liquidation mechanism helps maintain the $1 peg even during crypto market stress.

These designs offer more decentralization than fiat-backed versions. No central company controls the issuance process. However, they can be complex to understand and remain vulnerable to extreme crypto market crashes that overwhelm the collateral buffers.

Commodity-backed stablecoins

These digital assets tie to physical goods like gold rather than fiat currency like the us dollar.

Specific examples include PAX Gold (PAXG) and Tether Gold (XAUT). Each token represents a small fraction of a gold bar stored in secure vaults. The companies managing these assets provide regular audits of their physical holdings.

The value relationship works differently here. If gold’s market price moves, the token’s dollar value moves too. So it stays “stable” relative to gold, not to a fixed $1 amount. This appeals to people who want exposure to commodity prices in digital form.

These remain niche products compared to dollar-pegged versions. They serve investors who want gold exposure without physical storage hassles. However, they require trust in vault storage, insurance, and the company managing the underlying assets.

Practical considerations include storage costs, audit expenses, and redemption processes for physical goods. Users need to understand how to convert tokens back to actual gold if desired, and what fees apply for such conversions.

Algorithmic stablecoins

Algorithmic designs try to maintain a $1 price mainly through code and incentives, often with little or no traditional reserves backing them.

The most famous failure was TerraUSD (UST) in 2022. This stablecoin lost its peg completely, crashed far below $1, and wiped out tens of billions of dollars in value. The collapse showed how quickly confidence can evaporate in algorithmic systems.

The basic mechanism works through supply adjustments. The system increases or reduces the number of coins in circulation to push the price back toward $1. Some designs use a partner token to absorb volatility and provide incentives for stabilization.

Why are these risky? If confidence breaks and many holders try to exit simultaneously, no real reserve exists to support the price. The algorithm can spiral downward as selling pressure overwhelms the stabilization mechanisms.

Because of these spectacular failures, many regulators now treat algorithmic stablecoins more like speculative crypto assets than stable digital money. Some jurisdictions have banned or restricted their use following the UST collapse and similar incidents.

What are stablecoins used for in practice?

Beyond trading, stablecoins increasingly support everyday financial needs. People use them for payments, international transfers, and protecting savings from inflation.

The most important real-world applications include:

- Trading crypto without constant volatility

- cross border payments and remittances at lower cost

- Protecting savings in high inflation economies

- Business payments and humanitarian aid distribution

Concrete examples show their impact. Argentinians used dollar stablecoins heavily during 2023’s hyperinflation exceeding 200%. Turkish citizens turned to them during lira instability. NGOs in parts of Africa use stablecoins to distribute aid more directly to recipients.

Stablecoins move over public blockchains, so transfers often clear in minutes or seconds. Even on weekends and holidays. This speed advantage over traditional wire transfers appeals to both individuals and businesses with urgent payment needs.

However, users still need smartphones, internet access, and basic digital literacy. They must also protect their private keys or wallet passwords - lose these, and the money is gone forever.

Trading and “parking” value between volatile cryptos

Traders regularly move into stablecoins when they want to step out of volatile positions without fully cashing back to their bank accounts.

Here’s a simple scenario: Someone owns Bitcoin worth $10,000. Market news suggests a big price drop is coming. They sell Bitcoin for usd coin, holding the stable value. Later, if they choose, they can buy back Bitcoin at potentially lower prices.

Many crypto exchanges worldwide use dollar stablecoins as their main pricing unit. You’ll see trading pairs like BTC/USDT or ETH/USDC instead of traditional currency pairs. This creates a parallel financial system where funds rarely leave the crypto ecosystem.

Stablecoins help traders avoid the delays and fees of constantly moving money between traditional banking system accounts and exchanges. Instead of waiting days for bank transfers, they can move value instantly between different trading platforms.

Professional traders often keep significant funds “parked” in stablecoins between trades. This provides flexibility to act quickly on market opportunities while avoiding the stress of holding volatile crypto assets during uncertain periods.

Fast, low-cost cross-border payments

Traditional international transfers can take several business days and charge substantial fees through banks or remittance services. Stablecoin transfers often settle within minutes at lower cost.

Consider this cross-border example: Someone in Europe sends USDC to family in the Philippines using a mobile wallet. The recipient can convert to local pesos via a local crypto exchange or peer-to-peer platform. Total time: under an hour instead of 3-5 business days.

Stablecoins prove especially attractive for smaller remittances. Traditional services often charge high fixed fees that eat into small transfers. Blockchain networks typically charge low, flat fees regardless of transfer size.

These transactions travel over public blockchains like Ethereum, Tron, or Solana. The networks operate 24/7 without stopping for weekends, holidays, or banking hours. This continuous operation suits people who need to move money urgently.

Network choice matters significantly for user experience. Ethereum can be expensive during high traffic periods. Newer chains like Solana or Polygon often provide faster, cheaper alternatives for the same stablecoin transfer.

Hedge against weak or high-inflation currencies

In countries where local money loses value quickly, people sometimes use dollar stablecoins to protect their purchasing power.

Argentina provides a clear example. During 2023’s hyperinflation exceeding 200%, USDT adoption surged 50% year-over-year. Residents used dollar stablecoins for savings, business transactions, and everyday purchases to escape peso devaluation.

Similar patterns emerged in Turkey during lira volatility and in Venezuela during economic crisis periods. While holding dollar stablecoins carries its own risks, it can be more stable than local currencies losing value month after month.

People in high inflation economies often use stablecoins to:

- Store savings in dollar-equivalent value

- Pay for imported goods priced in dollars

- Conduct business transactions in stable units

- Send and receive payments without currency conversion risk

This behavior can affect local banking systems and capital flows. When citizens move savings into dollar stablecoins, it represents capital leaving the domestic financial system for digital alternatives.

Payments, business uses, and humanitarian aid

Freelancers and remote workers increasingly get paid in stablecoins to avoid international wire delays and high fees. Small businesses use them for supplier payments and customer transactions.

NGOs have found stablecoins useful for humanitarian aid distribution. In regions with weak banking infrastructure or capital controls, organizations can send funds more quickly and transparently to intended recipients.

Some merchants in emerging markets now accept stablecoins directly for goods and services. Customers pay using smartphone wallets and QR codes, similar to domestic mobile payment apps but with global reach.

Blockchain records provide transparency advantages. Organizations can track whether aid funds reached the right wallet addresses, creating an audit trail. While individual identities may remain private, the flow of funds becomes visible.

However, converting stablecoins to local currency for everyday spending often requires access to crypto exchanges or peer-to-peer marketplaces. This adds complexity compared to traditional bank transfers in well-developed financial systems.

Benefits and risks of stablecoins (in simple terms)

Stablecoins combine some benefits of crypto - speed, global access - with the familiarity of traditional money. But they also introduce new risks that users should understand.

Key Benefits:

- Speed: Transfers settle in minutes instead of days

- 24/7 availability: No banking hours or weekend delays

- Lower fees: Often cheaper than traditional wire transfers

- Global reach: Works anywhere with internet and smartphone

- Easy crypto trading: Move between volatile coins without bank delays

Primary Risks:

- De-pegging: Price can slip away from $1 during market stress

- Reserve questions: Unclear whether backing assets truly exist in full

- Cyber security: Hacked wallets or lost passwords mean permanent losses

- Regulatory uncertainty: Rules remain unclear in many jurisdictions

- Issuer failure: What happens if the company behind a stablecoin fails?

Real examples make these risks concrete. In March 2023, usd coin temporarily dropped to $0.87 when Silicon Valley Bank - which held some of Circle’s reserves - faced a bank run. Although USDC recovered quickly as the situation stabilized, holders faced uncertainty about their dollar claims.

The TerraUSD collapse in 2022 provides an extreme case. This algorithmic stablecoin fell from $1 to nearly zero in days, wiping out $40 billion in value. Many users lost their life savings because they misunderstood the risks of unbacked stablecoin designs.

Traditional bank deposits in developed countries carry FDIC insurance up to $250,000. Stablecoins generally provide no such protection. Users bear the full risk of issuer problems, market disruptions, or technological failures.

How stablecoins differ from bank money and CBDCs

From a user’s perspective, stablecoins can feel like digital cash. Behind the scenes, they work very differently from bank deposits and central bank digital currencies.

A bank deposit represents a claim on a regulated financial institution. In the United States, the FDIC typically insures deposits up to $250,000. Banks must follow strict capital requirements and undergo regular examinations by federal regulators.

A stablecoin is usually a claim on a private issuer or trust company. This entity is not the federal reserve system or other central bank. Reserve backing, insurance coverage, and redemption rights vary widely depending on the specific issuer and jurisdiction.

CBDCs represent a different approach entirely. A central bank digital currency would be digital money issued directly by institutions like the Federal Reserve or european central bank. This makes CBDCs the safest possible form of national currency - backed by the full faith and credit of the government.

Stablecoins generally exist outside the traditional monetary base. They don’t count as official money supply in most countries. Rules about interest payments, insurance, and legal redemption rights differ significantly across issuers.

Safety perspectives require careful research. Users need to understand: What specific assets back this stablecoin? Where are reserves held? What legal rights do holders have if something goes wrong? These details matter more than marketing claims about “100% backing.”

Regulation and the future of stablecoins

As stablecoins have grown into a hundreds-of-billions market, regulators worldwide have started building clearer rules for this new form of digital money.

The US establishing national innovation frameworks and the european union’s MiCA regulations represent detailed approaches to stablecoin oversight. These laws aim to ensure issuers hold safe reserve assets and follow anti-money laundering rules similar to other financial institutions.

Key regulatory developments include:

- Reserve requirements: Mandating safer backing assets like treasury bills

- Licensing: Requiring formal authorization to issue stablecoins

- Auditing: Regular third-party verification of reserve holdings

- Redemption rights: Clear rules for converting stablecoins back to fiat currency

- Cross-border coordination: International cooperation on regulatory standards

Singapore, hong kong sar, UAE, Japan, and other financial centers have introduced or updated frameworks between 2022 and 2025. Most focus on licensing stablecoin issuers and setting minimum standards for reserve management and operational controls.

Some jurisdictions take different approaches. Mainland China has effectively banned stablecoins, focusing instead on its digital renminbi CBDC project. Other countries remain in wait-and-see mode, studying developments before committing to specific rules.

Looking ahead, expect more licensed, fiat-backed stablecoins from traditional banks and payment companies. These will likely operate under stricter rules but offer stronger consumer protections. tokenized money market funds may emerge as regulated alternatives to current stablecoin designs.

The genius act and similar legislation suggest governments see stablecoins as part of the future payment infrastructure. Rather than banning them, most developed countries are working toward frameworks that balance innovation with financial stability and consumer protection.

Closer coordination between regulators will likely emerge to manage global capital flows and prevent regulatory arbitrage. As stablecoin adoption grows, cross-border consistency becomes more important for both issuers and users.

Discover how we use stablecoins in our safe investment strategies.

Stablecoin FAQ for Beginners

What is a stablecoin?

A stablecoin is a type of cryptocurrency designed to stay close to a steady value, usually equal to one US dollar. Unlike Bitcoin or Ethereum, which can change price very quickly, stablecoins aim to reduce price swings. This stability is often achieved by linking the coin’s value to something familiar, such as traditional money, commodities, or mathematical systems.

Many people view stablecoins as a bridge between traditional finance and crypto because they combine blockchain technology with more predictable prices.

What are the top 5 stablecoins?

While rankings can change over time, the most commonly known stablecoins are:

- USDT (Tether)

- USDC (USD Coin)

- DAI

- BUSD (Binance USD, now less active)

- TUSD (TrueUSD)

These stablecoins are widely used for trading, payments, and moving funds within the crypto ecosystem. Popularity is usually based on market size, usage, and availability across exchanges.

What is the best stablecoin to stake?

Some stablecoins are commonly used in staking or earning programs on certain platforms. Coins like USDC, DAI, and USDT are often involved because of their wide adoption.

It is important to understand that returns, rules, and risks depend on the platform or protocol being used, not just the stablecoin itself. Staking or earning mechanisms are part of decentralized finance and come with their own considerations.

What are the four types of stablecoins?

Stablecoins generally fall into four main categories:

- Fiat-backed stablecoins

These are backed by traditional currencies like the US dollar. Each coin is meant to represent money held in reserves. - Crypto-backed stablecoins

These are backed by other cryptocurrencies. Because crypto prices can fluctuate, extra collateral is often required. - Algorithmic stablecoins

These rely on code and supply adjustments rather than direct backing. They aim to keep prices stable through automated mechanisms. - Commodity-backed stablecoins

These are backed by real-world assets such as gold or other commodities.

Each type works differently and carries different levels of complexity and risk.

Is Bitcoin a stablecoin?

No. Bitcoin is not a stablecoin. Bitcoin’s price can rise or fall significantly in short periods of time. Stablecoins are specifically designed to maintain a steady value, while Bitcoin is designed as a decentralized digital asset with a limited supply.

Are stablecoins good for beginners?

Many beginners find stablecoins easier to understand compared to highly volatile cryptocurrencies. Because their value is usually tied to something familiar, they can feel more predictable and less overwhelming.

That said, stablecoins are still part of the crypto market and involve technology, platforms, and systems that may take time to learn.

What stablecoins have failed?

Some stablecoins have lost their intended value in the past. A well-known example is TerraUSD (UST), which collapsed in 2022 due to weaknesses in its algorithmic design.

These events highlight that not all stablecoins work the same way, and stability is not guaranteed in every model.

How risky are stablecoins?

Stablecoins are generally less volatile than many cryptocurrencies, but they are not risk-free. Risks can include:

- Issues with reserves or transparency

- Platform or smart contract failures

- Regulatory changes

- Design flaws in certain stablecoin models

Understanding how a stablecoin works and what supports its value can help one better grasp the level of risk involved.

Related Posts

Why stablecoins deserve a place in your portfolio

.png)

.png)

Bitcoin and Ethereum allocation: how much to hold

Core-satellite crypto portfolio strategy explained

Never miss another article

Sign up to our email list to receive monthly newsletter.